In mid-December of 2021, the Federal Reserve announced that they are prepared to fight inflation with as many as three interest rate hikes — starting as early as February of 2022 — in an effort to cool persistently high inflation. Its benchmark rate, which affects borrowing and lending for things like new homes or new cars, has been near zero since the start of the pandemic in a bid to boost the recovery.

But with recent inflation causing widespread concerns, the Fed is planning to raise rates to hopefully keep consumer goods prices in check.

“Over time, as the Fed raises interest rates, consumers should see somewhat higher interest rates for mortgage loans, for car loans, and businesses should see maybe some tighter terms to obtain financing,” explained Julia Coronado, former economist for the Fed.

So what does that mean for someone looking to buy a new home in 2022?

In short, it means act fast. Buy now. Avoid paying more for the same home… or worse, end up with a smaller, older home because the one you really want is suddenly out of your budget.

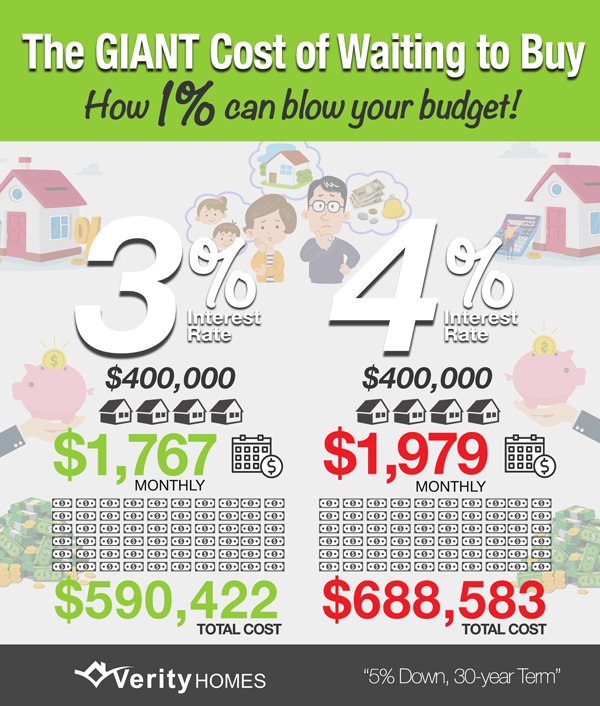

Home prices don’t rise and fall with changing interest rates. What DOES change is your monthly payment. In other words, the exact same house — with the same selling price — is going to cost you more per month when the interest rates go up. The home you want right now (and can afford right now) may be out of reach as soon as the rate hikes take effect.

Appreciation: Another Cost to Waiting

Interest rates are not the only factor you need to consider when trying to figure out when is the right time to buy a new home. If you’re like most home buyers, you probably pay most attention to home prices… and you’ve probably noticed them going up a lot in recent years.

Real estate appreciates, which is why home ownership has always been a cornerstone of “The American Dream.” Home ownership is an investment that grows, and the numbers prove it. So that $400,000 home you have your eye on right now is only going to get more expensive the longer you wait to buy it.

Again, while the obvious thought buyers have is to wait for the market to calm down — and hopefully see home prices fall — historical data on home values prove that’s a false hope. Barbara Corcoran (of “Shark Tank” fame) explains:

“I don’t think it is wise to wait,” Corcoran said. “Of course, if you can’t find a house, you have to wait. But to make it part of your plan to wait until house prices come down, I don’t envision that happening over the next few years, at least not for the next year.”

Bottom line for Corcoran — and based on the data — is that waiting to buy is going to cost you money:

If US home price appreciation maintains a pace similar to the past year, she said, homebuyers are going to pay another 12% to 14% for the same house next year. Goldman Sachs recently forecast home prices would increase by another 16% by the end of 2022.

Inevitably, the hot housing market has drawn comparisons to the 2006 housing bubble. But Corcoran does not think this is a bubble, because the high prices are not artificially supported by shady lending practices the way that sub-prime lending led to foreclosures during the last housing crisis and there aren’t a lot of flippers in the market.

“We don’t really have a bubble, what we have is an usual market that’s just gone bonkers based on individual demand of the people who want to live there,” she said. “I have never seen a housing market like this. I spent almost 50 years in the real estate business. I’ve never seen prices nationally go up at this kind of a rate.”

The reason for the price increases, she said, is a lopsided market, with overwhelming demand and historically low inventory. “You don’t have enough houses to go around.”

Meanwhile, mortgage rates are rising, which could further cut into affordability, Corcoran said.

“Mortgages are going up,” she said. “You might wait till next year, but you’re going to definitely pay more, in my opinion. And you’ll pay more [to borrow] your money. Your expenses are really going to ratchet up.”

Recent Comments